March 31, 2026 – The City of Chicago entered into two General Obligation bond sales on March 10, 2026. This report discusses aspects of recent bond ordinances, sales, and refinancing efforts by the City:

The City recently retired more than $300,000,000 of General Obligation bond principal thanks to ongoing refinancing efforts (more than $720,000,000 in total principal and interest savings in the next 20 years).

The City’s new bonds (Series 2026A and 2026B) are taxable because they are funding operating expenses (retroactive Fire Department pay, and police settlements).

These bonds have relatively short turnaround dates for their principal due, and add more than $120,000,000 in annual bond expenses to the 2027, 2028, and 2029 budgets as currently constructed (without additional refinancing).

These bonds change the shape of the City’s current General Obligation payment schedules.

These bonds “eat” more than $655 million of the previously established bond payment savings mentioned above.

These future amounts owed may change, because the City plans at least two more bond issuances in 2026, for the purposes of implementing infrastructure; refinancing bonds; and implementing the Housing and Economic Development program.

We will follow these bond issuances, because it is anticipated that any refinancing will resolve some of the bulky near-term payments due over the next four years.

Residents should review the City’s bond issuance strategies for opportunity costs, to weigh the City’s total debt versus quickly implementing large programs like the 2024 – 2028 Housing and Economic Development Bond and Chicago Recovery Plan.

This report will discuss these points at length.

2026 Bond Updates

You may recall that during the 2026 Budget season, the City Council authorized two borrowing series for the City:

First, the City Council authorized the issuance of General Obligation bonds for the purposes of financing operating expenses (Fire Department contractual backpay and police settlements) in addition to traditional Capital Improvement Plan (CIP) spending.

Ald. La Spata was one of 11 alderpeople across a diverse range of caucuses who opposed this borrowing. Ald. La Spata raised concerns with the 2026 – 2027 CIP priorities, in addition to the typical municipal finance “no – no” of borrowing for operating costs.

Second, the City Council authorized the issuance of General Obligation or Sales Tax Securitization Corporation bonds for the purposes of refunding a series of outstanding bonds.

Ald. La Spata supported this ordinance, because refinancing bonds for savings is beneficial for the City and its residents.

In February 2026, MuniOS published a prospective issuance for several series of General Obligation bonds, including two series of taxable bonds (more than $500,000,000 under series 2026A and 2026G) and five series of tax exempt bonds (more than $290,000,000 under series 2026B through 2026F). Those issuance documents were then updated on March 18, as the City ultimately negotiated only two series of taxable General Obligation bonds ($511,925,000 under Series 2026A and 2026B) in their recent sale, instead of the previously proposed seven series.

The purposes of these bond proceeds are to pay costs associated with capital projects; to finance retroactive wage increases arising from collective bargaining negotiations (ex., Fire Department backpay); fund judgment and settlement payments; refinance outstanding amounts from one or more of the City’s credit lines; fund capitalized interest; and pay issuance costs.

2026A series bonds have three maturity dates, with the largest amount ($355,145,000) due January 1, 2031, and two subsequent due dates January 1, 2032, and 2033, respectively, to cover the balance of principal due.

$49,336,919.98 of proceeds will fund capitalized interest. The document states, “the City will not levy the Bond Property Tax Levies to pay the interest due with respect to the Series 2026 Bonds through January 1, 2028 which interest will be paid from the proceeds of the Series 2026 Bonds and interest earnings on such proceeds” (MuniOS, March 10, 2026).

$166,000,000 of proceeds will be used to fund “Retroactive Wage Increases” (Fire Department backpay).

$267,342,155.83 of proceeds will be used to fund settlements and judgments.

The cost of issuance is $2,945,924.19.

2026B series bonds have one maturity date, for $26,300,000 principal due January 1, 2032. These bonds will fund $23,358,657.64 of capital improvements; $2,779,054.93 of capitalized interest; and $162,287.43 of issuance costs. These bond sales are formally published on the City Clerk’s website as well:

The 1st Ward Office has studied these documents and compared payment structures to the 2025 General Obligation bond series, and believe the following needs to be studied further:

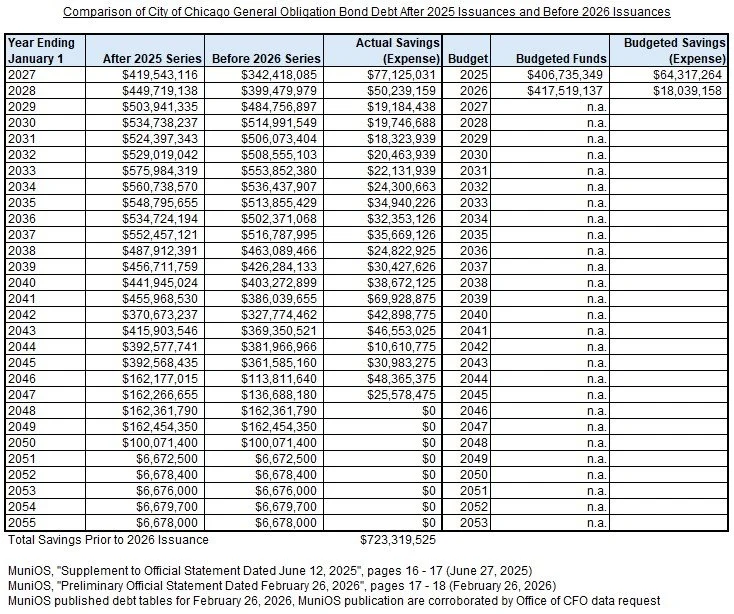

MuniOS documents suggest that between Q3 2025 and Q1 2026 the City refinanced more than $300,000,000 in bond principal, resulting in more than $720,000,000 in General Obligation bond principal and interest payments over the next 20 years (Table 1).

This is potentially a “virtual” savings situation for future City budgets.

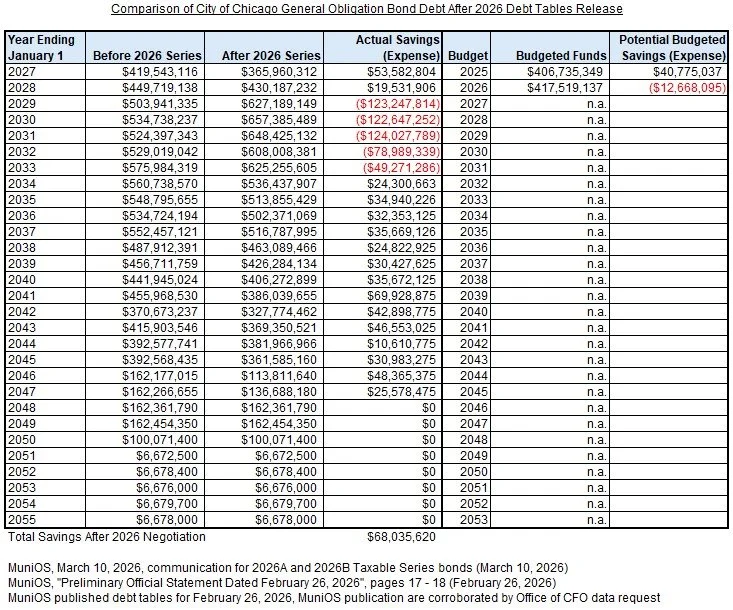

The 2026A and 2026B MuniOS documents suggest that the short-term principal due dates for the operating expenses bonds “cost” the City more than $655,000,000 in those aforementioned virtual savings (Table 2).

These amounts need to be studied further because the City is authorized to issue additional refunding bonds, as mentioned above, in conjunction with the 2026 bonds.

If the City does not further refinance additional General Obligation bond series that are owed in the next four years, the publicly released bond tables available on MuniOS suggest that the City will need more than $120,000,000 annually in each of the 2027, 2028, and 2029 budgets to cover the forthcoming 2026A and 2026B General Obligation bonds.

The City regularly refinances bonds between budget cycles, however, so it may not be surprising to see these amounts reduced in the future.

In addition to any Sales Tax Securitization Corporation refunding series that may be forthcoming in 2026 pursuant to ordinance, the City also intends to sell additional bonds for the following purposes:

Q2 2026, subject to market conditions: Fund Capital Improvement Plan projects; refinance Royal Bank of Canada credit (2024 ACFR pg. 262); and potential refunding certain general obligation bonds.

Q3 2026, subject to market conditions: implement aspects of the 2024 – 2028 Housing and Economic Development bond program.

Table One

Table Two

Bond Basics

When the City of Chicago issues General Obligation bonds, they are typically the result of a complicated negotiated sale process that involves numerous financial entities (banks and investment firms, for example) and trustees (established to manage payments between the City and bondholders).

The documents associated with bond sales are available for free on the website MuniOS, which publishes bond issuances of a variety of entities from across the USA.

These documents include detailed information about the City’s finances, sometimes more timely, granular, or targeted than what even comes across in the City’s budget process or audits, because these documents are meant to convey the City’s ability to repay its bonds (which is usually an excellent bet outside of some economic unrest in the late Nineteenth Century. Cf. Alberta Sbragia, Debt Wish: Entrepreneurial Cities, U.S. Federalism, and Economic Development, University of Pittsburgh Press [1996]).

The Chicago Public Library also has The Fundamentals of Municipal Bonds available if you’re interested in this topic (Neil O’Hara, Wiley [2012]). If you can locate a copy, The Handbook of Municipal Bonds (ed. Sylvan G. Feldstein, Frank J. Fabozzi; Wiley [2012]) also has many interesting contributions.

(I) Authorizations

What is tricky about the City’s bond issuances is that they do not follow the set schedule that the City’s typical comprehensive financial audit (typically published every June) or budget process (recently, September through December). Rather, the City Council authorizes bond issuances via ordinance, and the City’s financial officers are thereby allowed to issue debt within the parameters of State Law, City Ordinances, and all relevant federal laws, in addition to market timing.

This should not be viewed as a categorically good or bad thing, because working from one authorization ostensibly allows the City to move within the market when it is able to meet the most advantageous financial conditions.

A concrete example of why this can be an issue occurred in autumn 2024, when there was some City Council consternation regarding a brokered deal for the City to refinance debt and enter into a complex repurchase deal, which essentially allowed the City to repurchase its own debt with refinanced proceeds and thereby cancel more debt. City Council approval potentially impacted the timing of this deal.

Rather, residents should instead question any associated opportunity costs connected to delayed bond issuance. For example, the City Clerk filing published for 2026B taxable series General Obligation bonds notes that these bonds were issued pursuant to the Chicago Recovery Plan bond ordinance, which originally passed City Council in October 2021.

City Clerk filings, corroborated by correspondence from the City, demonstrate that prior to Taxable Series 2026B bonds, only $71,035,000 of the available $660,000,000 authorization for the Chicago Recovery Plan were issued four years after City Council approval.

Along with $1,887,000,000 in Local Fiscal Recovery Fund proceeds (American Rescue Plan Act funds), the City proposed to issue $660,000,000 in General Obligation bonds to fund “certain initiatives focused on economic development, property improvements, homelessness shelter infrastructure, telecommunications infrastructure, information technology, parks, and climate mitigation infrastructure” (CRP, pg. 15).

Residents should ask, if these $660,000,000 in proposed programming were not implemented via General Obligation bond (which still has more than 80% of its issuance capacity after Taxable Series 2026B), whether they were implemented with other funds, or not implemented. This is arguably an opportunity cost for the City if the development and recovery of Chicago following the shutdown era of the COVID-19 pandemic did not receive as much investment as it could have.

Similar issues relate to the City’s Housing and Economic Development bond program, for which less than $100,000,000 of the $1,250,000,000 authorization to invest in development initiatives. Once again, the question of opportunity cost should be raised with regard to lagging times for developing much needed housing and economic incentives.

(II) Refinancing

Throughout the current administration, as discussed previously on this blog, the City has aggressively refinanced its debt. The City has so aggressively refinanced its debt that general governmental bond principal (issued by the City and the Sales Tax Securitization Corporation, respectively) has not kept pace with inflation over the last decade.

Residents should not categorically view this as a good or bad thing, but rather ask specific questions about programmatic impacts (for example, discretionary ward infrastructure spending, commonly known as aldermanic “menu” money, has not been inflation adjusted once during Alderman La Spata’s terms in office, despite the fact that a May 2019 dollar is $0.22 short of a February 2026 dollar).

If the City has additional capacity to issue and refinance its bonds and thereby implement more infrastructure projects that improve the lives of Chicagoans, businesses, and tourists, or encourage growth, residents should question what a healthy level of debt actually looks like.

For example, during the 2026 Budget process, the original refinancing ordinance was cut from $2,000,000,000 authorization to $1,000,000,000 authorization.

If these refunding proceeds would have accelerated financing for more infrastructure projects, residents should question the balance between debt and investment.

Shifting the governmental bond burden to Sales Tax Securitization Corporation (STSC) has budgetary implications of moving bond obligations to sales tax, which in recent years easily has a reported balance above $900,000,000 annually (MuniOS; annual City Budget Ordinances – Corporate Fund Revenue, “Sales Tax Residual”); by contrast, General Obligation bonds are secured by property taxes. STSC bonds are not an obligation of the City, in contrast to General Obligation bonds.