Exploring Cash Governance

May 2026 – Despite reports of the City’s persistent annual budget gaps in the Corporate Fund in recent years, the City has greatly expanded its cash and cash equivalents and investment balances. This report reviews cash and investment practices, comparing those practices with City Budget Ordinances and audits where needed, to provide explanatory background that could help shape budget and investment policy proposals.

For governmental functions, the City held more than $1.7 billion in restricted and unrestricted cash in 2024, an increase of more than $750 million over the last decade.

For business functions, the City’s cash holdings fluctuated more on an annual basis than governmental cash, but overall the City held more than $1.9 billion in business cash in 2024.

For both governmental and business functions, unrestricted and restricted investments increased substantially over the last decade. In 2024, the City held more than $7.6 billion in investments across all functions.

Unrestricted government investments saw the largest increase ($2.7 billion) and restricted business investments saw the largest increase for that function ($1 billion).

Over the last four years the City Treasurer’s annual investments have exceeded budgeted investment expectations by more than $1 billion.

Over the last seven years, the City Treasurer has increased its investment pool by more than $1.9 billion.

These investment strategies include the investment of bond proceeds, which recently do not have any investment returns reported as available prior year surplus in the annual budget ordinance.

By comparing City’s audits, Treasurer’s Statements, and budget, it is possible to find structural budgetary policy improvements that do not involve taxes or cutting services.

Reviewing Cash Governance

As has been covered at this blog over the last year or so, the City faces numerous budgetary pressures that are creating persistent budget gaps in the Corporate Fund. These gaps typically live in the Corporate Fund because the Corporate Fund is the City’s “General Fund” for discretionary spending. This includes many of the common fees, fines, taxes, and other revenue sources that finance the everyday services Chicagoans depend on (Police, Fire, homelessness services, sanitation services, development functions, etc.). Despite the persistent budget gaps forecasted by the City on an annual basis over the last few years, outside of the budget the City has substantially improved its cash positions, and its annual investment strategies (TABLE 1, below).

Over the last decade, all restricted and unrestricted cash and cash equivalents (excluding escrow) for governmental functions increased more than 75% (or more than $750 million);

Business functions maintained relatively stable cash balances (business cash balances declined by roughly 4%, declining by $77 million to a total balance of more than $1.9 billion).

Over the last decade, all investments increased more than $2.8 billion for governmental functions and more than $1.45 billion for all business functions. Thus, in the 2024 audit, all restricted and unrestricted investments totaled more than $7.6 billion.

TABLE 1 – CASH AND INVESTMENTS, 2015 – 2024 (NOMINAL DOLLARS AS REPORTED ANNUALLY)

Source: Annual Comprehensive Financial Reports

Zooming in, here are some specific observations regarding the City’s cash and investments (TABLE 1):

In 2024, the City’s annual audit reported more than $1.5 billion held in unrestricted cash for governmental functions, and more than $400 million in unrestricted cash for business functions.

Over the past decade, the City’s annual audit has reported that unrestricted cash and cash equivalents increased for governmental functions by more than $680 million, while business functions remained relatively steady with a nominal decline of approximately $22 million in unrestricted cash.

Year-over-year, the City’s unrestricted cash balance for governmental functions declined by more than $1.1 billion between 2023 and 2024 (meaning that the unrestricted cash balance had grown to well over $2.7 billion by 2023).

Alderman La Spata and the 1st Ward office regularly query City budget and finance officials as to what the City “spent” more than $1 billion unrestricted cash on in 2024 (“spent” is in quotation marks because it is not entirely clear that these amounts have not simply been transferred into another beneficial asset category for the City; served some other payment function in lieu of property tax receipts; or served some other revenue replacement purpose, such as the missing Chicago Public Schools pension payment).

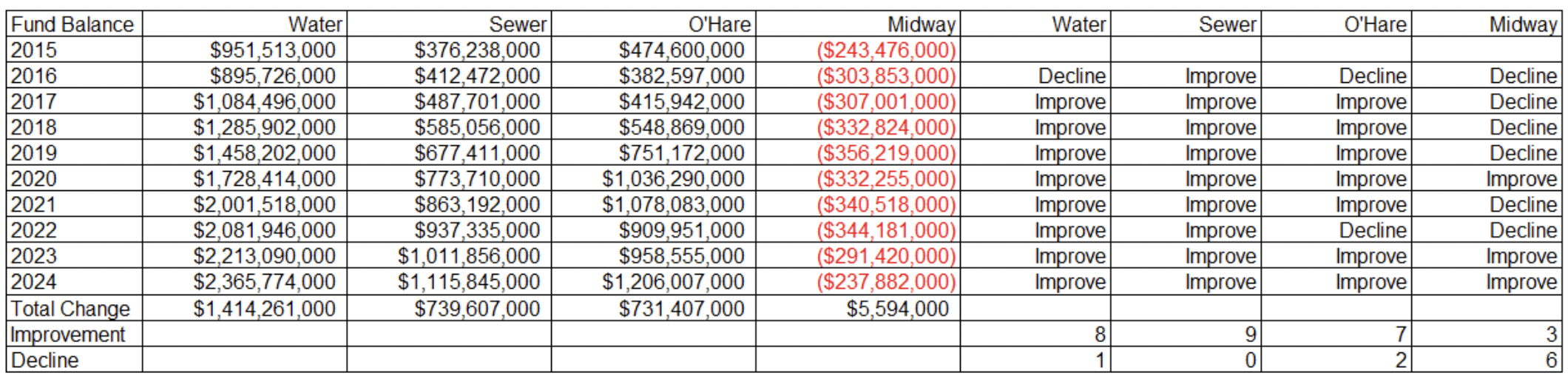

Year-over-year, the City’s cash balances for business functions are much more tumultuous than the cash balances for governmental functions, which should not categorically be assumed problematic due to the large capital expenditures that could be made for business functions in any given year, and due to the generally strong fund positions exhibited by the water, sewer, and O’Hare International Airport functions (see TABLES 2 AND 3, below).

Over the last decade, the City Water Fund balance increased by more than $1.4 billion. Both the Sewer and O’Hare Funds increased by more than $700 million.

The Water, Sewer, and O’Hare Funds only had three years in which their respective balances declined over the last decade.

Only the Midway Fund exhibited a persistently negative balance, and even this balance substantially improved over the last few years.

TABLE 2 – COMPARISON OF FUND BALANCES FOR CITY ENTERPRISE FUNCTIONS, 2015-2024

SOURCE: annual comprehensive financial audits

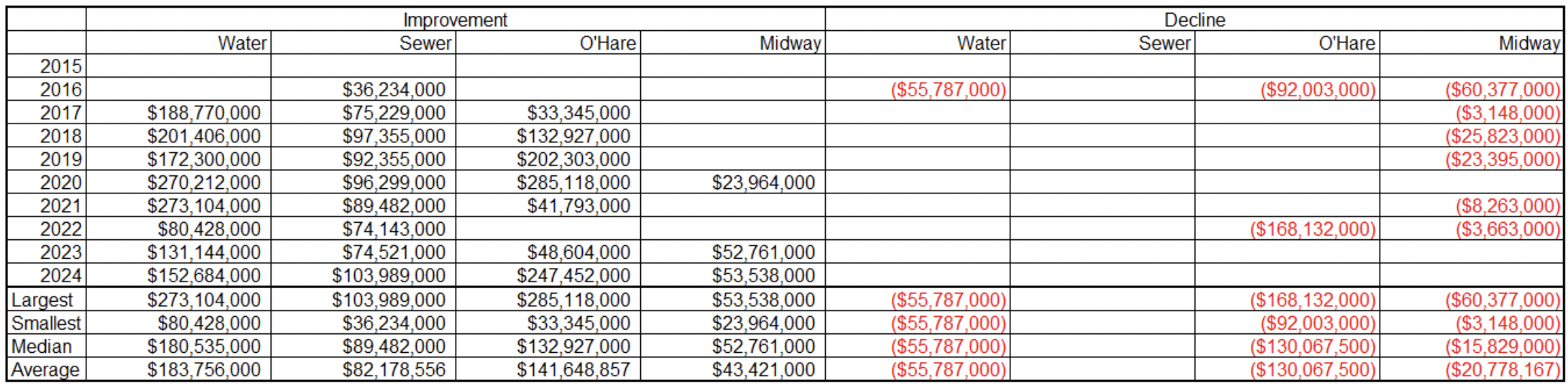

TABLE 3 – SPECIFIC ANALYSIS OF CITY ENTERPRISE FUND BALANCE, BY IMPROVEMENT OR DECLINE

SOURCE: annual comprehensive financial audits

In 2024, the City’s annual audit reported more than $170 millions held in restricted cash for governmental functions, and more than $1.5 billion held in restricted cash for business functions.

Over the past decade, restricted cash balances have not grown as much as unrestricted cash balances; this should be further examined to understand how the purposes of liquidity and specific “structures” for how money is owed define restricted cash (ex., bond payments are due July 1 and January 1; payroll is due twice a month; and so on).

In 2024, the City’s annual audit reported almost $3.5 billion in unrestricted investments held for government functions, and more than $600 million in unrestricted investments held for business functions. Restricted investments totaled more than $530 million for government functions, and more than $2.9 billion for business functions.

The City’s restricted governmental investments remained relatively flat over the decade, increasing only $22 million between 2015 and 2024, whereas the unrestricted governmental investments expanded by more than $2.7 billion during the decade.

Special attention should be paid to “Special Taxing Areas” here, as pages 38 and 39 of the 2024 audit demonstrate that special taxing districts comprise more than 62% of the City’s governmental investment balance.

By contrast to the governmental functions, the City’s business investments increased most for restricted investments, which grew more than $1 billion over the last decade, compared to $400 million growth for business function unrestricted investments.

In addition to all of these cash and investment holdings, the City also reported in its 2024 audit more than $760 million in cash and investments held with an escrow agent. Over the last decade, this balance has remained relatively consistent, which should be further investigated for its budgetary function (ex., cash held in escrow would likely be subject to very specific agreements and purposes).

The City’s General Obligation bond offering documents also note that there are trustees that serve the function of facilitating the collection of payments owed by the City and the distribution of any amounts owed to bondholders. These functions should be further researched and investigated for any potential budgetary, transparency, or reporting improvements.

In a communication through the Chair for the February 2026 Committee on Finance meeting to review City depositories, the City acknowledged that its cash and cash equivalent balances increased due to a number of reasons following the COVID-19 pandemic, including liquidity management.

If one reviews credit rating reports about the City of Chicago over the years, one can also find that credit rating agencies regularly discuss cash position or liquidity as a beneficial aspect of City management.

Thus, an increase in cash balances over the last decade should not categorically be met with skepticism or cynicism, but it should be further scrutinized against the City’s annual budget gaps to determine where and how certain sources of excess investment returns or other forms of beneficial revenue can be returned to the Corporate Fund to structurally bolster budgetary operations.

In addition to scrutinizing any potential budgetary and financial implications of the City’s cash and investment management, one may consider normative arguments about the function of City services. Any budgetary or financial study could be colored by assumptions about who specific or ideal constituencies are for City services, and whether the City’s primary responsibility is to protect itself and its standing as a Municipal Corporation, or prioritize outward development and services.

Budgeting Investment Income

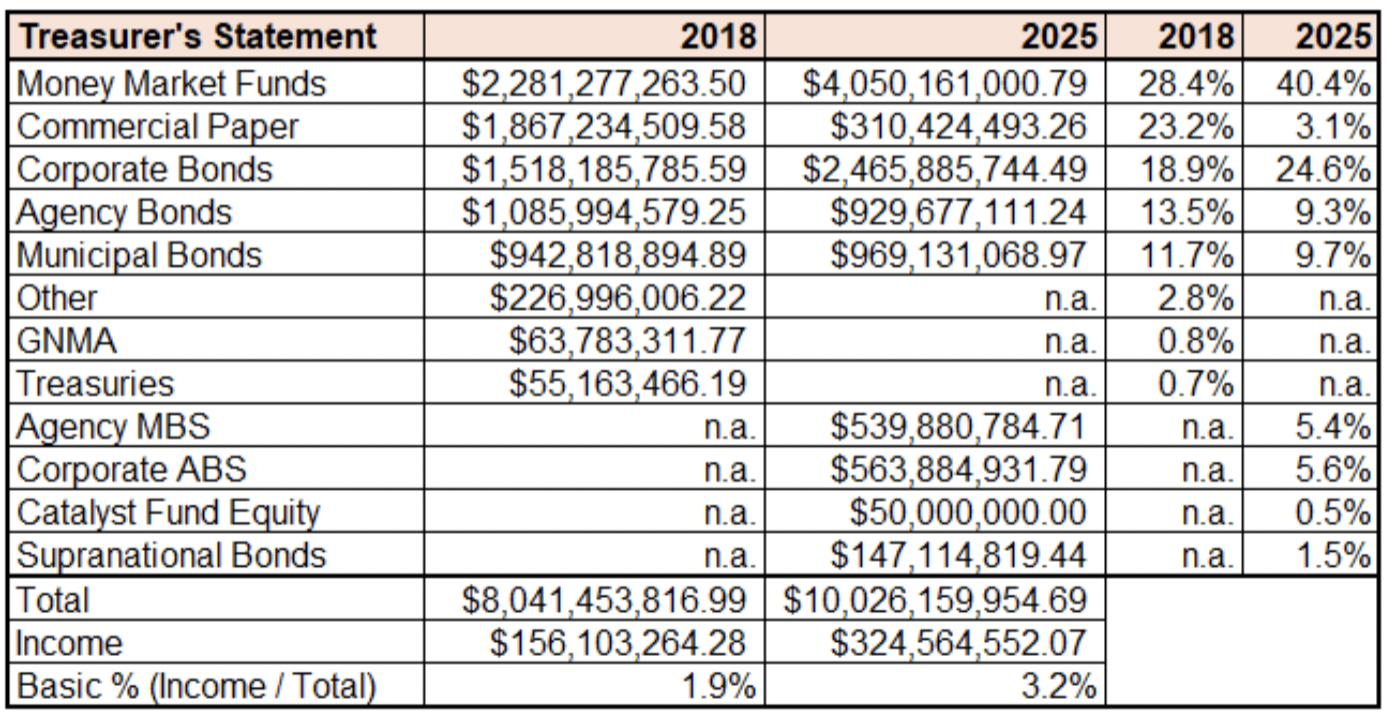

Alongside the recent increase in cash balances, over the last four years the City’s Treasurer has taken great advantage of the relatively high interest rate environment (as compared to the “Quantitative Easing” years, or the late 2010s), and over the last eight years shifted their fixed income investment blend. As TABLE 4 shows (below), the City Treasurer substantially increased the basic return in 2025 (stated solely as a percentage of income versus total investment amounts) compared to 2018:

TABLE 4 – COMPARISON OF CHICAGO TREASURER’S OFFICE STATEMENTS, 2018 AND 2015

SOURCE: F2019-17 cto 2018 statement

f2026-0022758, cto 2025 statement

categories are replicated directly from cto and defined by their investment policy

In a communication through the Chair of the Committee on Finance for the February, 2026, meeting on City depositories, the City explained that the Treasurer’s reported investment income is reflected in the budget not as a single centralized revenue line, but rather is allocated according to the specific funds to which those investments belong (for a very basic example, if the City Treasurer invested $3, $2 of which were from the Corporate Fund and $1 from the Water Fund, investment returns would be allocated and budgeted according to that split).

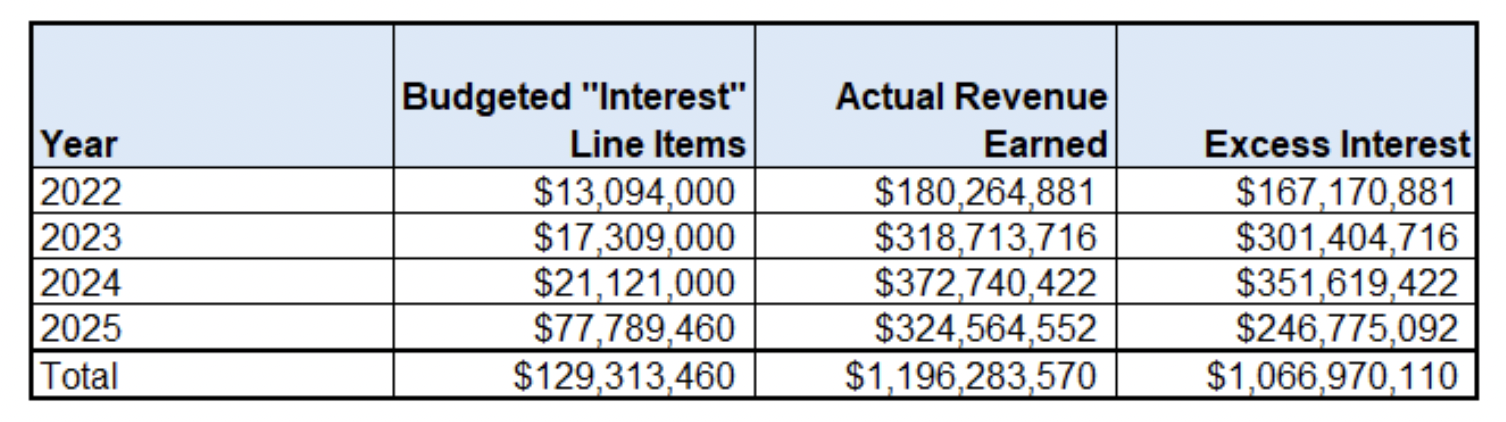

Further investigation is needed for this practice, because over the last four years the City Treasurer’s actual investment returns substantially exceed the budgeted amounts for either the preceding, current, or following year (TABLE 5).

TABLE 5 – COMPARISON OF BUDGETED “INTEREST” LINE ITEMS AND ACTUAL TREASURER INVESTMENT RETURNS

SOURCE: CITY BUDGET ORDINANCES (FINAL); CTO STATEMENTS

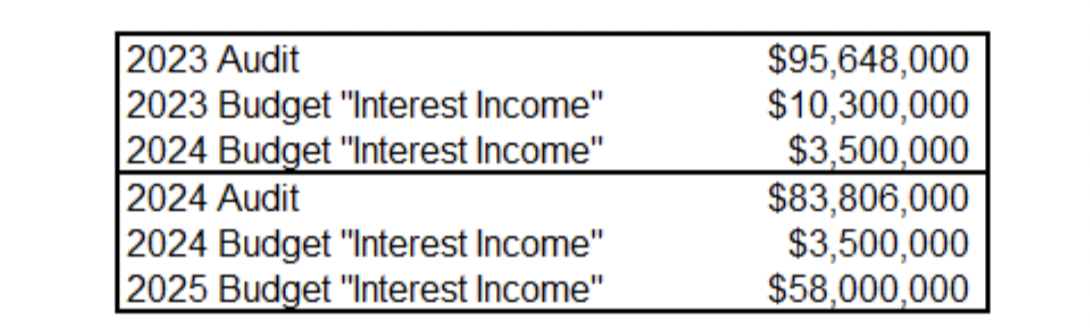

What is important to note is that when one disaggregates investment returns by Fund, as published in the City’s audit, the corresponding returns following a given year (say, 2023 actual investment returns) are not the amount that appears in the corresponding budget (say, 2024 budget). TABLE 6 below demonstrates how 2023 and 2024 investment returns reported for governmental functions in the General Fund compare with the respective current year budgets (2023, 2024) and subsequent budgets (2024, 2025).

TABLE 6 – COMPARISON OF INVESTMENT RETURNS WITH BUDGET

SOURCE: ANNUAL COMPREHENSIVE FINANCIAL REPORT

FINAL BUDGET ORDINANCES (PUBLISHED)

It should not necessarily be surprising that the City does not carry forward excess investment income in the Corporate Fund: as discussed at length here, the General Fund is the City’s discretionary revenue fund for City services and its revenue sources are generally not legally restricted. Therefore, in the event that one revenue source exceeds its budgetary amount (say, licensing fees), the City would simply pocket that revenue and either apply it to any budget surplus; any excess expenditures; or, to supplement any lost revenue.

Most commonly, in recent years news reports on expenditure overruns would focus on settlements and overtime, for example; and, most prominent lost revenues in recent years are due to Chicago Public Schools’ failure to make their promised pension payment to the City, and the declining Personal Property Replacement Tax revenue from the State of Illinois.

Thus, on one hand, (1) it is possible to simply conclude that the City’s improvements in its investment program, even if that improvement is solely attributed to the higher interest rate environment of recent years, serves as a much-needed cushion to maintain liquidity in the midst of other budgetary pressures.

(Of course, one could counter this statement by scrutinizing the budgetary performance of specific line items, as available in each annual audit.)

On the other hand, (2) (a) it is possible to review the ongoing increase in available investment revenues and (b) the overall improvement in investment performance, and thereby question whether or how some of these excess investment returns can be returned to specific budgetary purposes (such as Prior Year Available Surplus).

Regarding (2)(a), TABLE 4 demonstrates that the Treasurer’s investment base increased more than $1.9 billion in 2025 compared with 2018; Regarding (2)(b) TABLE 5 shows that actual investment income exceeded budgeted amounts by more than $1 billion between 2022 and 2025.

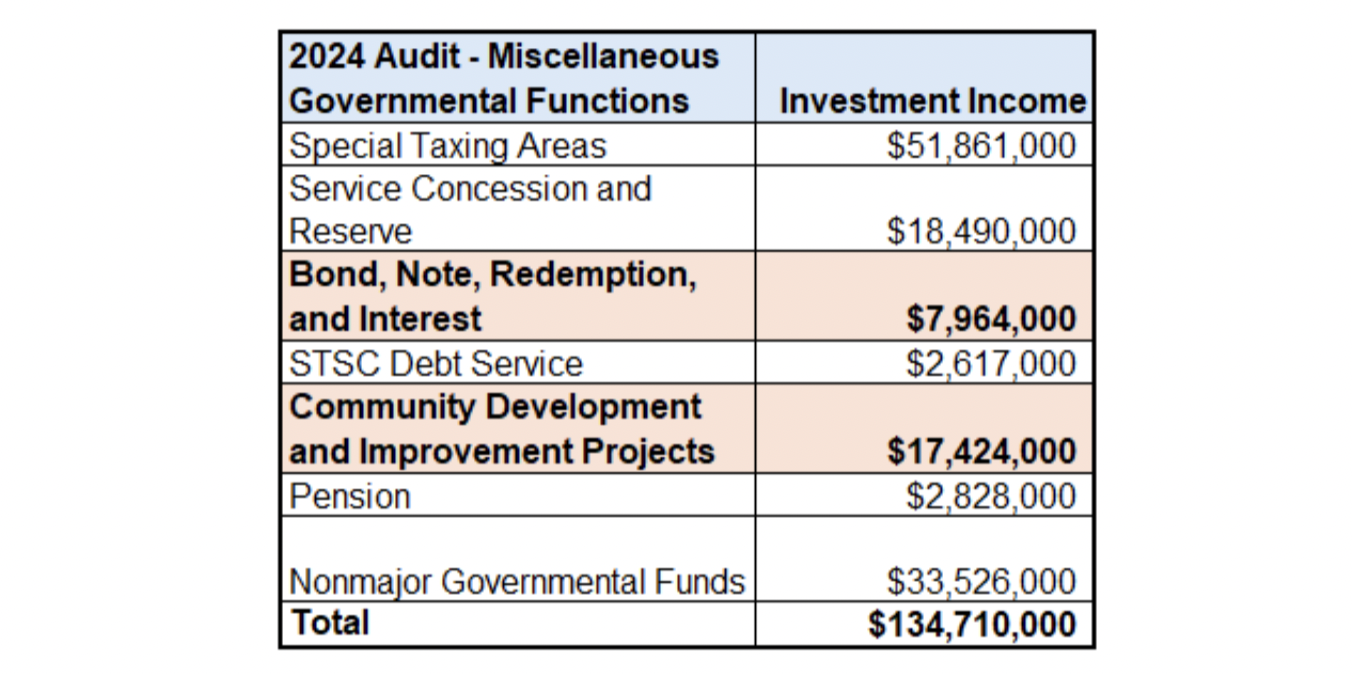

To accomplish this second task, one can use the 2024 audit reports on investment income by fund to discern where investment income has exceeded budgeted amounts outside of the General Fund. This is arguably a more helpful analysis, because each fund outside of the General Fund is solely intended to serve specific legally defined purposes, and would require a legal budgetary transfer to demonstrate if those revenues were used by any other fund. TABLE 7 below demonstrates several miscellaneous government functions from the 2024 audit that do not neatly correspond to budgeted funds; let’s focus on bonds and infrastructure (highlighted).

TABLE 7

The City’s General Obligation bonds are serviced out of the Bond Redemption and Interest Series Fund, and in recent budget ordinances there is no such thing as a Community Development Fund, Improvement Projects Fund, or any other combination of those words. By definition in the audit, the Community Development and Improvement Projects Fund is associated with the bond debt used for infrastructure development (these plans are available on a quasi-annual basis via Capital Improvement Programs) and “to acquire property, finance construction, and finance authorized expenditures and supporting services for various activities” (ACFR 2024, page 57).

In 2024, the City earned nearly $8 million on investment income associated with its General Obligation bonds. This should not be surprising, as in numerous hearings and other correspondence over the last several years, the City’s financial officers regularly discussed investing bond proceeds while awaiting productive use. Yet, in the 2025 Budget Ordinance, the City reported no prior balance for the Bond Redemption and Interest Series Fund (PDF page 5) nor reported any miscellaneous revenue sources (Budget 9 / PDF page 32).

One should ask why revenue earned by the City via investment of its bond proceeds (a perfectly legitimate practice while awaiting productive use) is not reported as balance in the Bond Redemption and Interest Series fund, particularly because the property tax levy leverages bond issuances. Any additional revenue reported in the budget would ipso facto reduce property tax proceeds or Corporate Fund subsidy needed for bond payments.

In general, the 2025 (PDF pages 5 – 6) and 2026 (PDF pages 5 – 6) Budget Ordinances did not uniformly include prior year surplus or deficit balances for each and every fund. It is worth researching this practice further, because the “shape” of many funds changes over time (for example, Budget Ordinances over the last five years have changed how revenue sources are named and reported for the Bond Redemption and Interest Series fund).

In 2024, the City earned more than $17 million on investment income associated with Community Development and Improvement Projects. This should not be surprising, as the City typically uses massive bond outlays to finance infrastructure and development, as defined in the City’s audit (Community Development and Improvement Projects Fund solely corresponds to bond proceeds for those purposes).

As noted above, one should ask why these additional investment returns are not reported as balance in the Bond Redemption and Interest Series fund, or aggregated as separate revenue line items.

By researching cash management and investment returns, alongside the budget documents and capital planning documents, it is possible to find potential budget improvement practices related to the City’s financial practices. 1st Ward residents regularly contact the office with issues or concerns about increasing or creating numerous taxes each budget year, and also discuss issues with City Services (for example, requesting changes to the street sweeping schedules; more frequent street sweeping; more frequent tree trimming; and so on) or the need to cut spending.

Scrutinizing the City’s financial apparatus outside the budget reveals that there are potentially other paths forward on substantive revenue sources; this should not be construed as an argument that maintaining cash liquidity is not important, nor that the City should not be investing its funds;

Rather, this should be construed as an argument that the City can more thoroughly review the relationship between its actual financing apparatus and budget apparatus, to find structural changes that return more investments and cash to the budget where legally feasible and fiscally responsible.